After it was announced that federal student loan payments would resume last October, we asked borrowers to share their thoughts about the transition. What they had to say revealed widespread confusion, anxiety, and fear.

But how have borrowers fared since then? Here’s what we learned when we surveyed borrowers on the financial and emotional impacts they’ve faced in the months that have passed since the return to repayment:

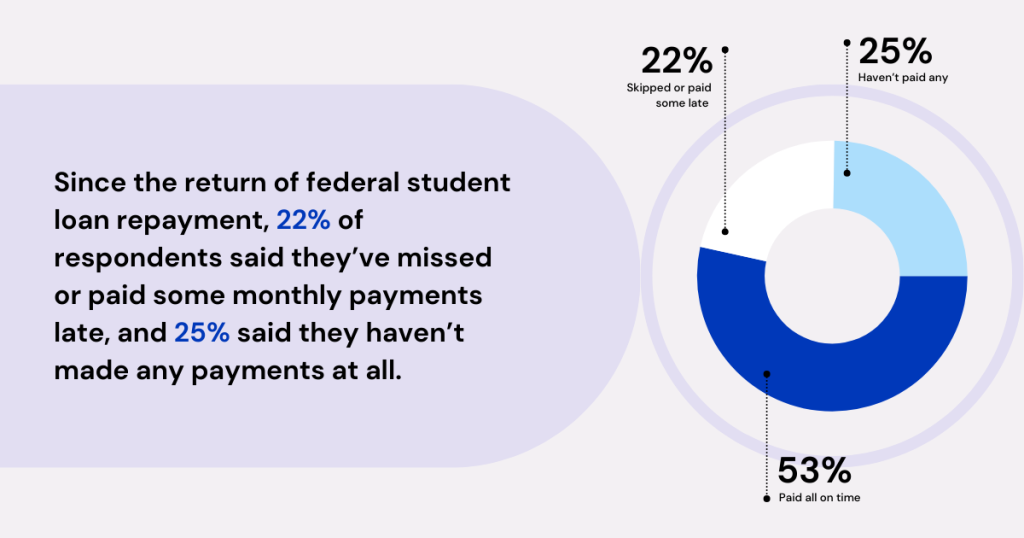

Almost half of respondents are struggling to make their monthly payments.

In the months since the return of repayment, 22 percent of respondents said they’ve skipped or paid some of their student loan bills late, and 25 percent said they haven’t made any payments at all — despite two-thirds (66 percent) of respondents reporting that they’ve enrolled in an Income-Driven Repayment (IDR) plan, which are intended to make monthly payments more affordable.

Thanks to an on-ramp period that will remain in place through September 30, 2024, borrowers are shielded from the usual ramifications of missed payments, such as going into default, being reported to credit bureaus, and being sent to collections. However, the on-ramp period doesn’t pause interest accrual, and borrowers relying on this temporary reprieve risk running into hefty consequences after the period ends.

“I can’t afford my income-driven payment amount — it’s too high. I have been unable to make any payments and it’s paralyzing me with fear.”

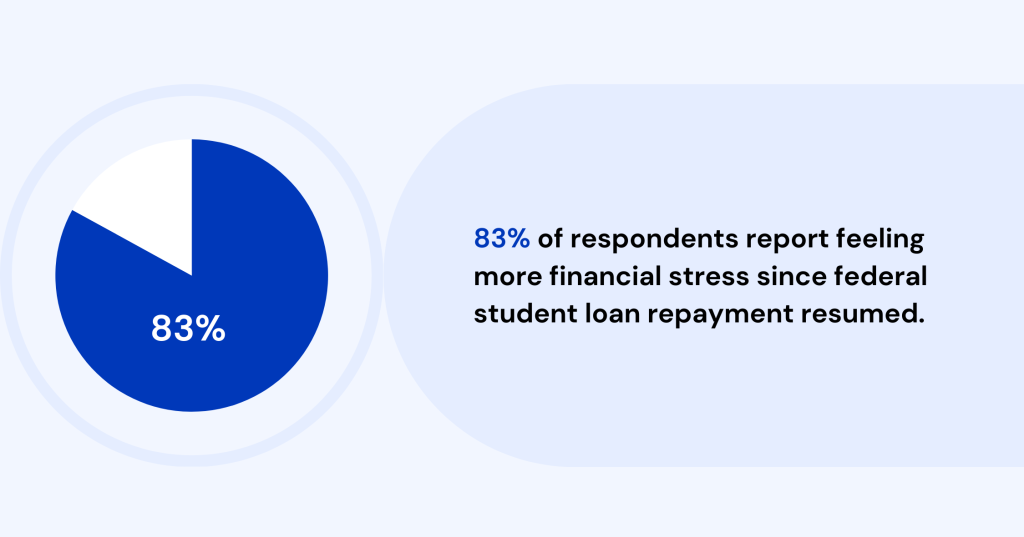

For most, financial stress has risen.

83 percent are experiencing more financial stress since the return to repayment — and among those respondents, more than three-quarters described feeling “much more” stressed. Given the far-reaching impacts the transition has had on borrowers, this finding is — unfortunately — unsurprising.

“It is already so expensive to try and get by, and adding a bill that’s $600-$800 a month has drastically increased my stress levels.”

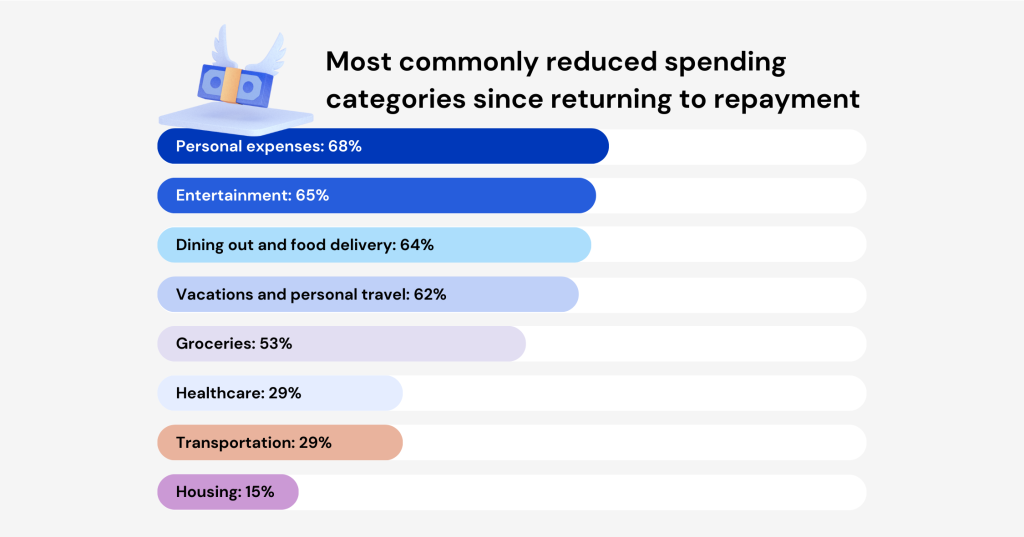

Spending and savings have taken a major hit.

83 percent of respondents said they’ve reduced their spending since the return to repayment. While personal expenses, entertainment, dining out, and personal travel rank as the most commonly reduced categories, a concerning number of respondents reported being forced to reduce spending on essential expenses, including groceries (53 percent), healthcare (29 percent), and housing (15 percent).

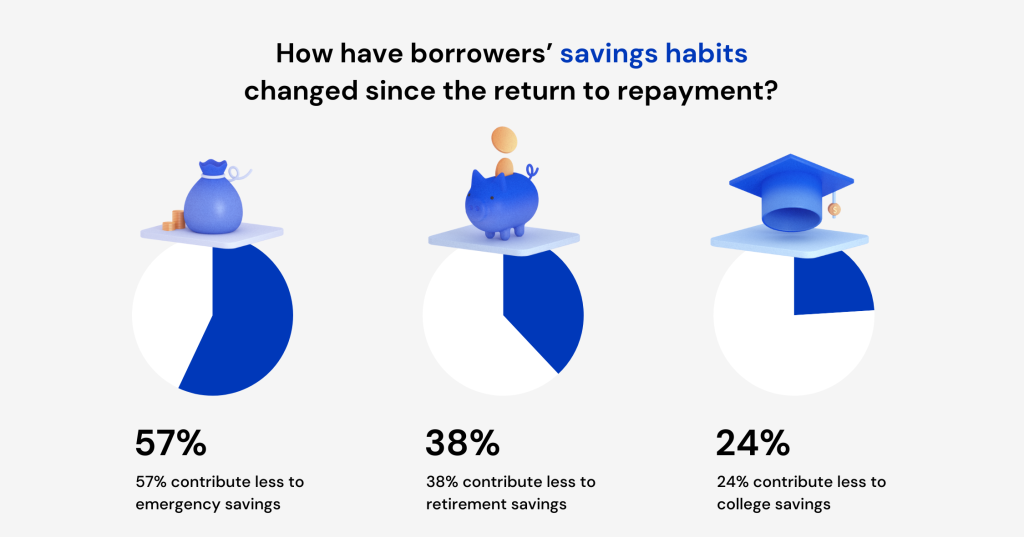

And it’s not just day-to-day spending that has taken a hit. Over half of respondents (57 percent) reported contributing less to their emergency savings, more than a third (38 percent) have scaled back their retirement savings, and around one in four (24 percent) say they’re putting less into their college savings accounts. Even more concerningly, 23 percent of respondents said they don’t have any savings in the first place. These trends all point to the potential that the return of federal student loan payment will have long-term — and serious — financial wellness consequences.

“It has absolutely ruined me financially. I can’t save a dollar, even though I’m only paying the minimum required on my loans.”

“Once repayment started again, we went from paying down debt, planning on getting a car, and investing to having to budget for basics.”

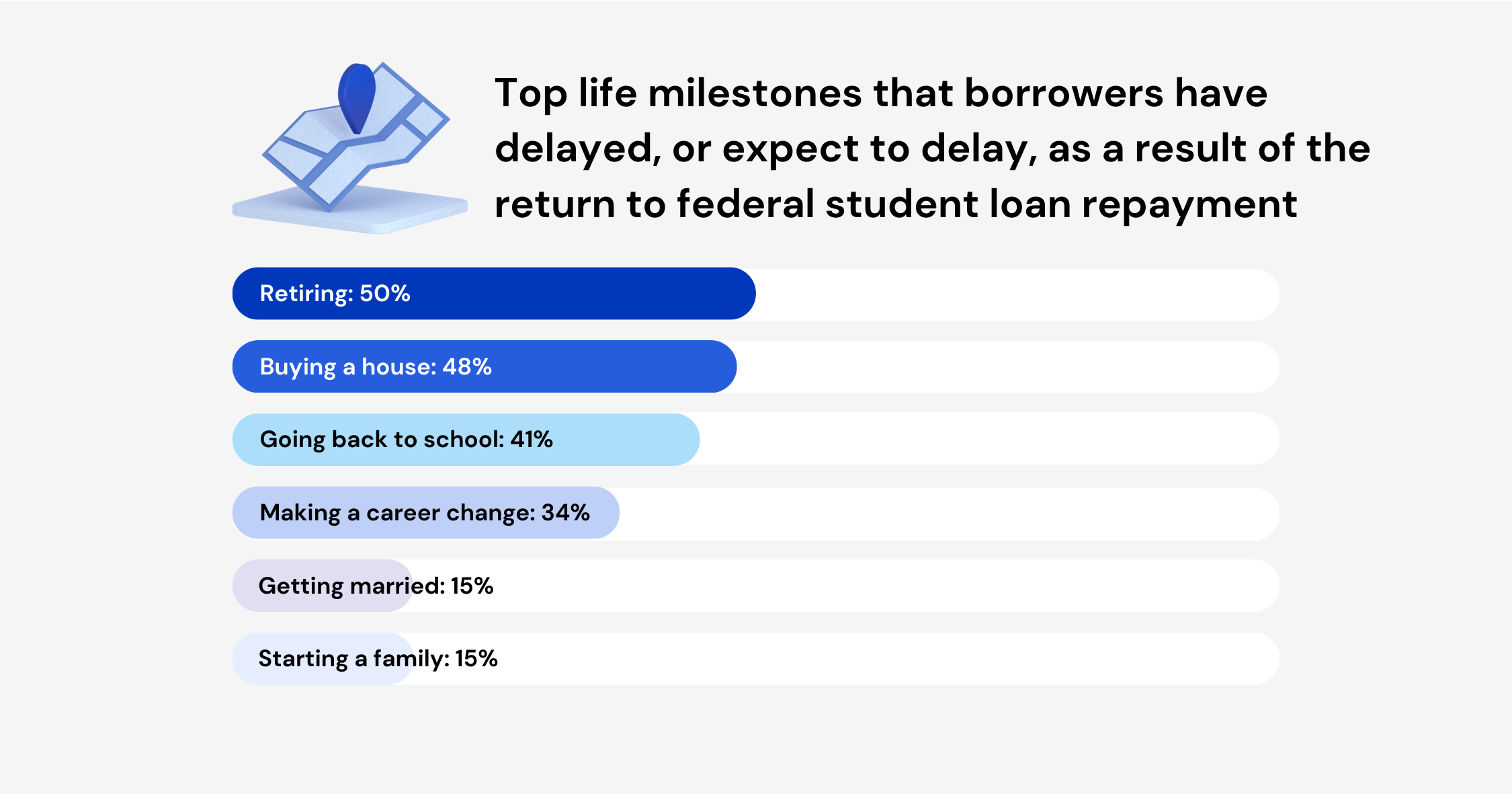

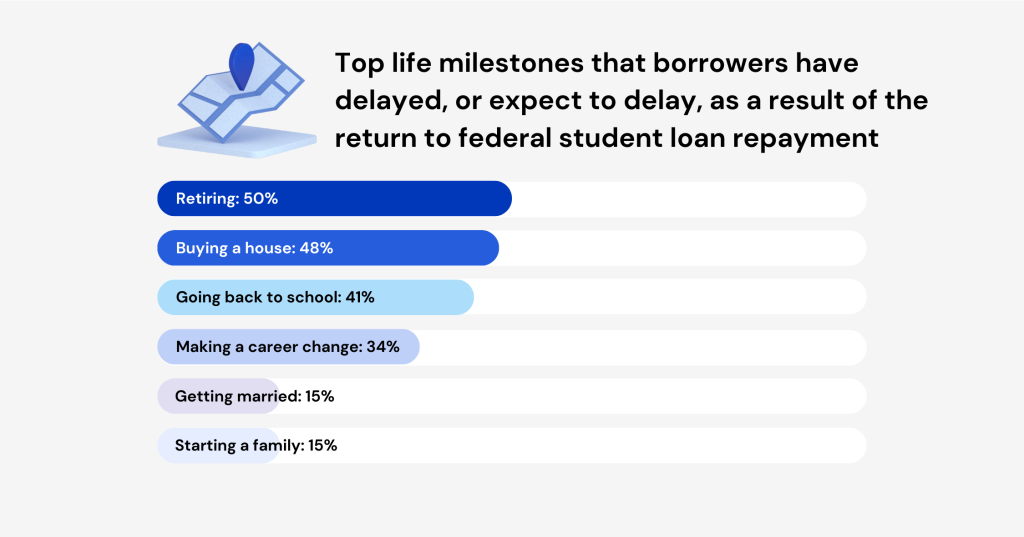

Many expect to delay personal milestones as a result.

For many, the impacts of this transition are more than just wallet-deep. Half of all respondents said they expect to push back retirement as a result of the return to repayment, 48 percent said they’ll have to delay becoming a homeowner, and 41 percent will have to wait to go back to school. Respondents are even rethinking their timeline for getting married and starting a family, with 15 percent delaying one or both of these milestones.

“My balance just keeps going up. It feels like I’ll never pay this off.”

There’s still an urgent need for help.

Our survey findings make it clear that borrowers need help. And the best channel to deliver that help: the workplace.

Why?

- Student debt stress hinders productivity and engagement. Prior to the return to repayment, one in three borrowers admitted that their personal finances are a major distraction at work — a figure that has surely increased since payments resumed.

- Financially stressed employees are more likely to quit. The return to repayment has sent financial stress levels skyrocketing — and that could lead to skyrocketing turnover costs, too.

- Without student debt support, the return to repayment is poised to derail DE&I initiatives. Women and people of color are more likely to borrow to pay for school, borrow more, and stay in debt longer. In turn, these groups are likely to be struggling more amid the return to repayment — at home and at work.

With Candidly, employers can offer benefits that provide immediate support while also setting employees up for sustainable, long-term financial health, resilience, and wealth. Our best-in-class student debt and savings platform makes it easy to design a program that reaches every employee, no matter where they are in their financial journey, with solutions and services including:

- Student Loan Repayment Contributions, which offer direct support to employees with student debt

- SECURE Act 2.0-friendly Student Loan Retirement Matching, which helps employees stay on track for retirement security while simultaneously paying off college debt

- Coaching services, through which employees can meet one-on-one with a certified student loan expert for personalized guidance

- Public Service Loan Forgiveness tools, which empowers eligible organizations to automate and streamline their PSLF application and review process